Leonardo S.p.A ($LDO.MI)

Global defense prime with accelerating fundamentals trading at a ~20% FCF yield.

EDIT: Closed this out at EUR 29.59 (a +150% return) on Feb 12, 2025.

Investment Thesis Summary

I believe that an investment in the common shares of Leonardo S.p.A. (trading in Milan, ticker: $LDO.MI) is compelling for the following reasons:

An improved backdrop for defense spending is set to drive an acceleration in revenue and earnings for Leonardo over the next 3+ years.

Free cash flow generation is set to meaningfully improve as the company’s Aerostructures segment reaches breakeven in 2025.

The recent listing of Leonardo’s US segment through a combination with RADA will serve as a catalyst to highlight the company’s severely discounted value.

A new incoming CEO is likely to remove key investor concerns surrounding Leonardo’s current CEO, Alessandro Profumo.

Leonardo will create value for equity holders by focusing on debt paydown as its number one priority.

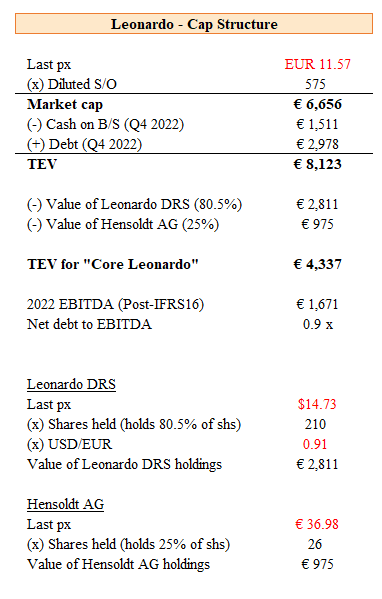

Capital Structure

Business Background

Leonardo SpA, originally known as Finmeccanica, is an Italian multinational defense, security, and aerospace business with headquarters in Rome, Italy. The company generated 14.7B EUR in 2022 and 1.2B EUR in EBITA, making it the eighth-largest defense contractor in the world.

Leonardo has the following principal business lines (all figures as of FY22):

Core Leonardo

Helicopters – Revenue of 4.6B EUR, EBITA of 415M EUR (9.1% margin)

Leonardo is a top 3 global player in the helicopter market.

Revenue is generated through helicopter design and production (c. 60% of revenue) and customer support and training (c. 40%).

Mix: 74% defense & government, 26% civil.

Flagship products: 15-seat medium class AW139 + AW169 + AW189

Aircraft – Revenue of 3.1B EUR, EBITA of 421M EUR (13.6% margin)

Leonardo is a top 5 global player in aeronautics.

Designs, develops, produces and provides logistic support for trainers, combat, and tactical transport aircraft including unmanned systems.

Key programs include the Typhoon Fighter, F-35, and GCAP (previously known as Tempest).

Defense Electronics & Security (DES) – Revenue of 4.7B EUR, EBITA of 553M EUR (11.7% margin)

Leonardo is the #1 player in defense electronics in Europe.

Designs, develops, and manufactures a wide range of products and systems for defense and security applications. Solutions include combat and mission management systems, tactical unmanned systems, radar, electronic warfare, optronics, infrared search, etc.

Aerostructures – Revenue of 0.4B EUR, EBITA loss of 189m EUR (-40% margin)

Produces and assembles major structural components for commercial aircraft such as the Boeing 787 Dreamliner, and the Airbus A220 and A321.

Segment still well below pre-COVID levels and has been a consistent drag on earnings and free cash flow.

Publicly traded subsidiaries and investments

Leonardo DRS (80.5% owned by Leonardo SpA; trades in the US as $DRS) – Revenue of $3.0B USD, EBITA of $265M (9.8% margin)

Leonardo DRS was recently formed through the merger of LDO’s DRS division and Rada Electronics (RADA) at the end of November 2022, with the company just having its first public earnings call in March 2023. The combined entity began trading at $11.50 per share (current price of ~$15) with a roughly ~$3.0B market cap. Leonardo SpA owns 80.5% of the company, with the rest of it owned by public investors.

Hensoldt AG (25% owned by Leonardo SpA; trades in Germany)

Leonardo SpA recently acquired a EUR ~600m stake in the publicly listed German company with the aim to establish a presence in the German defense market and to collaborate in the development of defense electronics.

Thesis

With an improved backdrop in defense spending, Leonardo is set to experience accelerating revenue growth and profitability over the next 3+ years.

Defense spending is set to increase meaningfully in markets such as:

Europe - expected to be the fastest-growing defense market (~5% CAGR est.) as countries ramp up spending in response to the Russia/Ukraine conflict.

Increases in budgets: Multiple countries committed to increasing their spending, with Germany targeting 2% of GDP by 2023, France targeting 2% by 2025, the UK targeting 3% by 2030, Italy targeting 2% by 2028, and Poland targeting 4% by 2023.

Formation of special budgets: Germany formed a one-time EUR 100B fund to revamp its military.

United States – increasing tensions with China and the need to support the Ukraine conflict are driving greater spending in defense (Leonardo DRS, the company’s US subsidiary, should benefit)

Increases in budgets: On March 9, 2023, the Biden Administration submitted to Congress a proposed FY 2024 Budget request of $842 billion for the Department of Defense, an increase of $26 billion over FY 2023 levels and $100 billion more than FY 2022.

Ukraine support: Since the conflict began, the US has sent close to $50B in additional (through appropriations) military aid ($18B in security assistance, $24B in weapons and equipment, $5B in grants and loans for weapons). Weapons and equipment sent to Ukraine will also have to be replaced.

Other geographies

Japan – Increasing its planned military spend to 2% of GDP by 2027 up from roughly ~1% now as the threat of China destabilizing the region looms large.

Two years ago, the company set a medium-term goal of mid-single-digit (MSD) revenue growth (from 2022 to 2026) and a high-single-digit (HSD) EBITA CAGR. Despite the breakout of the Ukraine/Russia war and the significant increase in orders, the company maintained this top-line guidance for 2023, with the sell-side still anchoring to this guide, which I believe will prove to be overly conservative.

In the last two quarters, Leonardo saw an acceleration in orders (on a TTM basis) to +16% YoY in Q3 and +21% YoY in Q4. Despite this, management has repeatedly communicated that they have yet to see any meaningful incremental orders placed from expanded government budgets. While governments can move at a glacial pace, the reality is that Europe will spend significantly more on defense and this will translate into accelerating revenue and profitability as the company works through its existing backlog.

Leonardo will see improved free cash flow generation as the civilian markets for aircraft recover and the company works through a series of one-off charges. Improving FCF conversion is likely to lead to a multiple re-rating.

Incremental EUR 300M in free cash flow generation as Aerostructures recovers.

Through its Aerostructures segment, Leonardo produces and assembles major structural components for commercial aircraft such as the Boeing 787 Dreamliner, and the Airbus A220 and A321. During the pandemic, as travel was halted, orders for new planes were meaningfully reduced, particularly for wide-body planes (which are traditionally larger and used for international travel). Even worse, the production of the 787 Dreamliner, which is a big driver of the segment’s revenue/earnings, faced defects and regulatory issues that halted deliveries. This had a large impact on the segment, with production volumes for the 787 decreasing to ~20% of 2019 levels. The Aerostructures segment has been a meaningful drag on performance, with a 2022 EBITA loss of ~190m EUR but a drag on free cash flow of ~300m EUR. Positively, Leonardo expects volumes to recover to about 80% of 2019 levels by 2025 and for the segment to reach breakeven.

Restructuring and non-recurring charges are finally set to decline in FY23.

Given the weakness in the Aerostructure segment, Leonardo has undergone a series of restructurings over the past two years which have been a EUR ~200m drag to free cash flow. The company expects that these payments will begin to taper down starting in FY2023.

Poor free cash flow conversion has been one of the main reasons why investors have shied away from Leonardo in the past. For instance, over the past five years, free cash flow conversion (as a % of EBITA) has averaged ~30% (excluding 2020). However, with improvements in profitability, the reduced drag from Aerostructures, and an end to a series of one-off charges, the company is on a credible pathway to improve FCF conversion to ~70%. I believe that this should drive a multiple re-rating as investors begin to see that Leonardo is actually cheap on a free cash flow basis and not just on a headline multiple.

The recent public listing of Leonardo DRS (November 2022) through the merger of RADA in the US will serve as a catalyst for investors to start properly valuing the remaining “core” business.

Leonardo is quite inexpensive on a fully consolidated basis, trading at 7.0x EBITA on 2022 numbers. However, once you net out Leonardo’s publicly traded subsidiaries and investments, you realize how cheap the opportunity really is.

Currently, Leonardo is trading at a total enterprise value (TEV) of EUR 8.1B. Its investment in Leonardo DRS (210m shares) is currently worth EUR 2.8B; Leonardo’s investment in Hensoldt AG is worth another EUR 1.0B. If we subtract these out, we can see that the “Core Leonardo” business is trading at a value of EUR 4.4B. However, the core business is set to generate at least EUR 800m of free cash flow in 2024 and likely close to 1.0B in 2025 (excluding Aerostructures).

While Leonardo has always been cheap relative to peers, the recent “backdoor” listing of Leonardo DRS, which was done with less publicity than the typical IPO, now allows investors to set a real mark on Leonardo’s US assets. With this real mark, it is now hard to ignore just how cheap the remaining business really is.

The replacement of LDO’s current CEO should remove a key governance concern and make LDO investable again.

Leonardo’s current CEO, Alessandro Profumo was accused and found guilty of fraud (for using derivatives to hide losses) during his tenure as Chairman at Tuscan bank, Banca Monte dei Paschi di Siena. Profumo was sentenced in 2019 and is currently on appeal. The company, however, has maintained its support for him, despite protests from investors, including activist Bluebell Partners.

On April 12, 2023 the Italian government appointed Roberto Cingolani as the next CEO of Leonardo.

While Profumo has not been accused of any impropriety while at Leonardo Spa, I do believe that many funds have likely passed on investing in the company (or perhaps, weren’t able to get past an investment committee) due to his fraud conviction. Cingolani’s appointment will thus be welcomed by investors.

LDO’s debt profile is more manageable than investors give it credit for. Moreover, the company’s number one priority of paying down debt will create meaningful value for equity holders.

Debt is optically high due to IFRS accounting:

Leonardo presents its net debt at ~3.0B EUR. However, this includes EUR 570m in leases and EUR ~700m in financial debt to MBDA (one of its JVs); the debt to MBDA is purely an accounting construct, in which excess cash that gets disbursed to JV partners is accounted for as debt. Since I consider leases expenses (and not debt), I think the “right” debt figure to use is EUR ~1.7B, which is slightly under 1.0x leverage – very manageable, in my opinion.

Leonardo’s key capital allocation priority is to pay down debt. This should create meaningful value for equity holders, with at least EUR ~600m in capacity per year for paydown. At a total enterprise value (TEV) of EUR 8.2B, the debt paydown generates > 9% return per year for the equity (plus interest savings).

A key point of pushback from European investors will soon become a non-issue: European investors often push back on Leonardo for carrying “too much” debt relative to other European defense peers. However, the fact is that “true debt” is quite manageable and could be paid down in its entirety within the next 2-3 years.

Valuation and Model

You can see my valuation of Leonardo above. I am valuing Leonardo’s core business at a 15x FCF multiple on my 2025 estimates. Defense peers have recently re-rated to a median multiple closer to 20x NTM EPS. I assume that Leonardo will be able to close the gap but not fully, hence the discount. I believe, over time, Leonardo could be worth north of 30 EUR/share vs. the current 12 EUR/share.

A quick note on valuation:

There are different ways to treat the Aerostructures segment as it is not currently profitable. The most “intellectually consistent” way would be to capitalize Aerostructure losses for a few years and then value the business on a normalized basis. Pre-COVID, the business was generating roughly EUR 1B in revenue. At a 5% EBITA margin, you might argue that the business is worth ~400m EUR (8x EBITA), which should be roughly equivalent to the losses that I expect from the segment over the next couple of years. For this reason, I exclude losses and essentially write down to Aerostructures to zero.

I haven’t taken much of a view on Leonardo DRS and Hensoldt AG and have just used their current market prices. While these are very good assets, they are not as clearly discounted vs. core Leonardo. However, I think any differences in the value of these assets are not going to be the biggest driver of returns here, which should be the core business + a re-rating.

Risks

An end to the Ukraine/Russia conflict would likely result in a sell-off and potential de-rating of European defense companies. However, I believe that European countries will continue to adhere to the increased budget given the risk of continued Russian aggression.

New CEO adds uncertainty around execution - new CEO Roberto Cingolani, who has previously served as Chief Technology & Innovation Officer at Leonardo, is set to be Profumo’s replacement. While Cingolani has experience working at Leonardo, he does not have CEO or capital allocation experience. Overall, however, his tenure should be a net positive for the stock given the negative optics surrounding Profumo.

Others: macro + energy costs + supply chain risks.

Any comments/feedback, please write to me on Twitter (@clarksquarecap). If you have enjoyed the post, please consider subscribing (for free!) below and sharing! Thank you!

greenwood just released their activist deck.

Interesting analysis. One question - in your valuation table, am I reading correctly that FCF (excl Aerostructure) higher than overall FCF? for e.g. in 2022, FCF is 298M vs FCF excl Aerostructure is 475M? This is despite Aerostructure currently being EBITA negative?