Quick Pitch #19

An attractive short-term setup with catalysts

EDIT: Closed this out at $30.68 on Jan 8, 2025.

Hello, Ultimate Value readers!

I am back with a new idea today.

This is more of a short-term trade than a long-term hold.

If my numbers are near the mark, I see ~50% upside, with solid near-term catalysts that could get us there quickly.

Liquidity is good, averaging ~$50m in ADTV.

Let’s take a look.

A month ago, I wrote a post titled “One to Watch Tomorrow” about Nebius—the shell of the former Yandex—which was set to begin trading again on October 21. With the stock halted for two years, I thought we might get to buy this grabbag of interesting assets for cash value.

Unfortunately, we did not get a shot at buying this then. My broker (IBKR) restricted trading the day of (due to Yandex’s prior Russia ties). The stock briefly traded down to cash value (~$13), but this was short-lived. Nebius closed at $20 that same day.

As I’ve continued working on this, I think the setup remains compelling. At $20.65, Nebius is a compelling short-term trade. Please note that this idea is HIGHLY speculative, so please size it appropriately.

To recap, what is Nebius?

In its current form, Nebius is a cash pile — $2.3B USD worth, to be precise — and a collection of businesses, which include:

Toloka – This business functions like an Amazon Mechanical Turk— where data-intensive, manual tasks can be outsourced to humans. This is valuable for creating data sets for AI training.

TripleTen – an educational boot camp that helps reskill workers.

Avride – focuses on driverless cars and delivery robots.

The core asset and primary driver of results is Nebius.

Nebius is an AI infrastructure company that provides access to high-performance computing resources (NVIDIA GPUs) and a wide range of value-added services to the global AI industry. It competes with Coreweave, Lambda, and others.

Currently, Nebius has 14,000 paid-for and deployed GPUs and expects to end CY24 with 20,000. The company expects to finish 2024 with an ARR of ~$180m (up from ~$120m in Q3). Its outlook calls for Nebius to reach the high end of $500-$1,000m in ARR by the end of 2025.

The Setup

The setup is compelling for the following reasons.

Nebius is a coiled spring — as funds stop selling their old YNDX shares, the stock will likely start to move.

Most funds with Nebius shares were prior owners of Yandex. Since Nebius is an entirely different proposition, most owners have been forced to sell their shares as it does not fit their mandate.

Nebius has 200 million shares outstanding, of which roughly 156 million represent the free float (excluding shares held by the founders + employees).

Since Nebius started trading in October, approximately 140 million shares have traded hands, representing ~90% of the float.

Given that the entire share register has almost turned over already, I believe the selling pressure will likely be over soon.

Sell-side coverage and estimates will likely come soon.

In this market, the best ideas are usually those you can’t screen for.

Nebius falls squarely into this category. Data service providers don’t have the correct historical numbers—Bloomberg, for instance, still has Yandex metrics under the Nebius ticker. Furthermore, the sell-side has yet to pick up coverage on the stock, so there are no estimates either. If you look at historical NBIS numbers, the opportunity won’t make any sense—$4B in market cap of $86m in revenue in the LTM?

This is not an IPO, but the sell-side usually has a quiet period of ~25 days before initiating coverage. It has been 29 days since NBIS started trading. This leads me to believe that the sell-side will start initiating coverage on the stock, which should improve investor interest in the story.

The valuation is still attractive. I see upside to at least $30 in per-share value.

Let’s take a high-level view here. Nebius will spend approximately $2.3B in CAPEX over FY23/FY24/FY25. At $30k per Nvidia GPU, that’s roughly 80k GPUS. Assume utilization of 70% (~7,000 hrs) and a leasing rate of $2/hour, which gets you to about $1.1B in ARR. Assume that’s closer to $1B for simplicity. During the Q3 earnings call, Nebius management stated that they will likely deliver above the mid-point of the $500 million to $1 billion ARR guidance range, which squares with the projection. Since Nebius is newer to the game, they will spend most of their CAPEX on the latest generation of chips, Blackwells, which should have better leasing rates (and better economics), especially while they remain scarce in the market.

GPU leases for large deals tend to show ~70% EBITDA margins or about 30% cash flow margins (over the length of the project) after power, space, labor, and depreciation. At a 30% cash flow margin, Nebius would generate ~$300m in cash flow.

What is the right price to pay here?

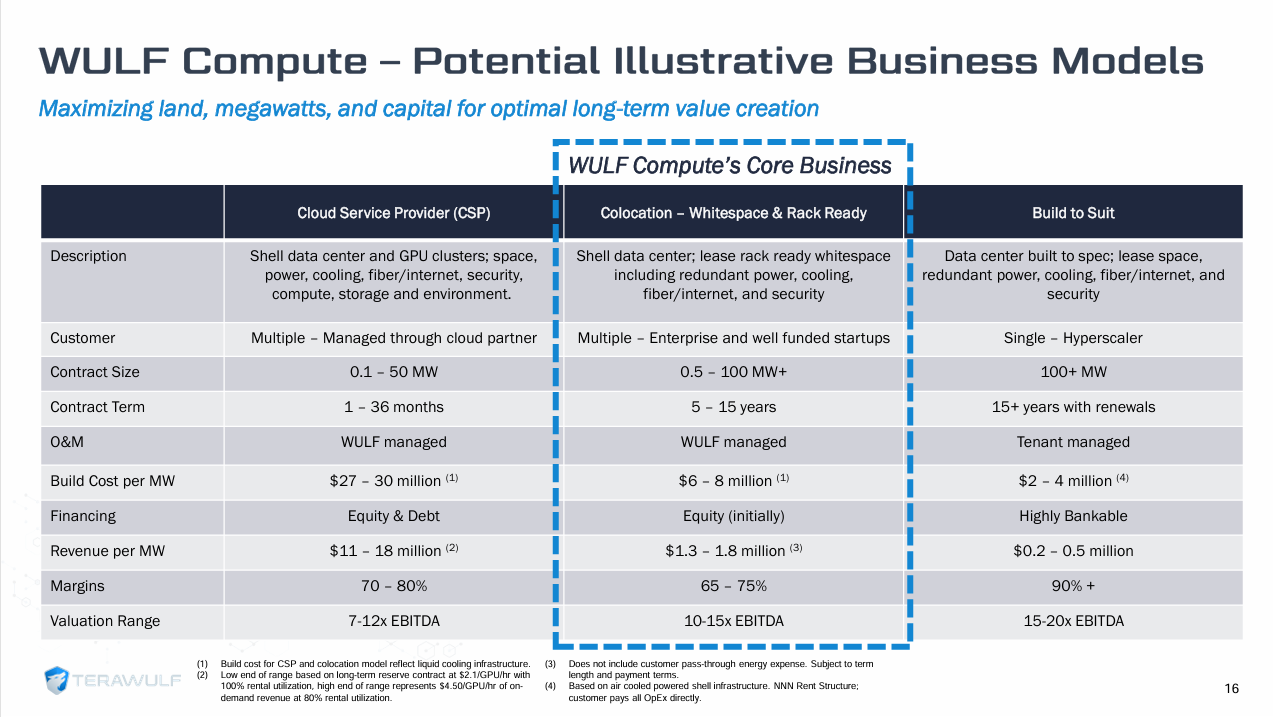

Perhaps a fair multiple would be somewhere in the range of 20-25x FCF, implying a fair value of ~$6-$7.5B, or about $30-$35 per share. As a sanity check, this backs into a ~8.5-11x EBITDA multiple, right in the ballpark of valuation ranges I’ve seen for these assets. See below, where crypto-miner/HPC player Terawulf laid out some different business model economics in their investor deck (on the left-hand side, under Cloud Service Provider).

There are MANY assumptions here, but at the current price (~$20, market cap of ~$4B), Nebius seems relatively inexpensive, even if you assume that the company spends all of its cash. That scenario might be too punitive, as GPUs (with contracts in hand) can now be financed with debt (see Coreweave + Blackstone).

You also have additional assets that could add a few more dollars in per-share value.

Clickhouse—a 28% stake last valued at $560m (assume this gets valued at 50%, and it is worth $1.50 per share).

Toloka— expected to be at $60m in revenue in 2025 with no CAPEX needs (at 1-2x revenue, this is worth ~$0.50 per share)

Tripleten- expected to be at $50m in revenue in 2025 with no CAPEX needs (at 1-2x revenue, this is worth another ~$0.50 per share).

AVride— with no revenue yet, it’s impossible to place a value on this.

Adding everything up should give us about $32.50-$37.50 in value.

Given the many assumptions, I will round it down to $30, which should still be roughly 50% upside from here.

Coreweave going public could drive a re-rating in the shares.

Earlier this month, Bloomberg reported that Coreweave (a main competitor to Nebius) is looking to go public and has selected Morgan Stanley, Goldman Sachs Group Inc., and JPMorgan to lead its planned initial public offering. This means that Coreweave is likely to file an S-1 soon, perhaps as early as December.

I think this could serve as a catalyst to 1) drive greater interest in the Nebius story, and 2) provide a more instructive view of the longer-term economics of the business, which would be a big positive given that Nebius is at a much earlier stage.

Putting it all together

There’s a lot to like here. Nebius is still in the $20 range ($20.65 at last close)—the same price it closed at during its first day of trading. While selling pressure has likely put a lid on the stock, this will dissipate soon. In addition, we should see sell-side initiations start to come through—and hopefully—a Coreweave S-1 within the next few weeks.

Importantly, you get pure-play AI (and autonomous driving!) exposure here at a valuation that is still anchored in reality, which is rare in the market today. While I’m not counting on any meme potential, I think the near-term catalysts should drive this higher. LONG.

Risks

Question marks regarding the unit economics of the business — there are many data points we don’t have yet (GPU leasing rates, utilization levels, electricity cost, space cost, building costs, GPU costs, etc) so it’s hard to model this with certainty.

Question marks regarding the value proposition — Nebius is a nascent business, so there are questions about why users would go to them vs. an established player like one of the hyper-scalers, etc.

The competitive environment could worsen — Nebius competes against much bigger and much better-funded competitors, including the hyper-scalers (Amazon, Google, Microsoft) and players like Coreweave, Lambda, and many others.

The unit economics could deteriorate — given the commoditized nature of GPU leasing, leasing rates could plummet, which would affect revenue/cash flows.

The Coreweave IPO could get pulled.

Thanks so much for reading! If you have comments/questions, drop by the chat thread below.