$TH - Investing in Target Hospitality

Recently signed transformative contract creates attractive risk/reward

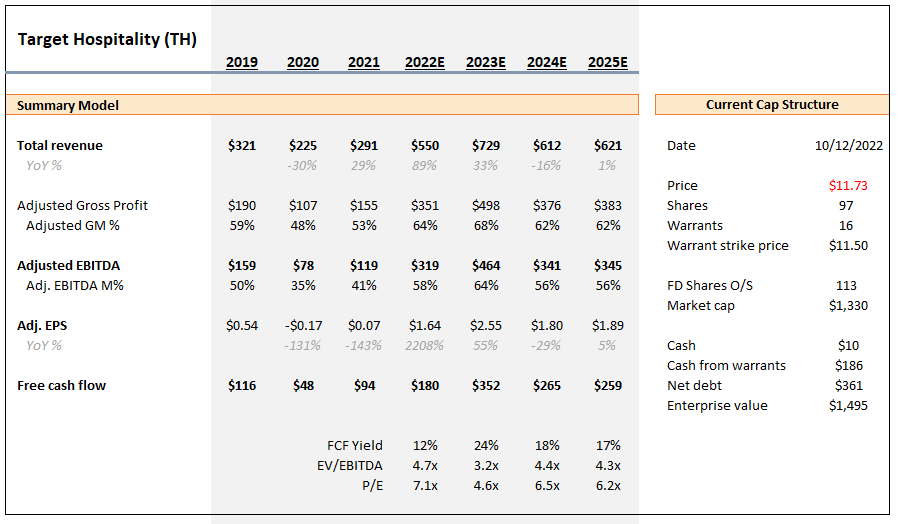

Date: October 12, 2022

Share Price: $11.73

FD Shares: 111m (including 16m warrants)

Market Cap: $1.33B

Enterprise Value: $1.50BInvestment Thesis Summary

Target Hospitality, a specialty rental provider of modular housing and services, recently signed a transformative government contract that raises its run-rate EBITDA to +$330m from prior guidance of $130m. Free cash flow generation should be meaningful given the low levels of maintenance capital required. I estimate that TH trades at an 18% FCF yield and 4.4x EBITDA on ‘24 numbers.

The new level of steady-state earnings will allow TH to pay down $340m in senior secured notes and reach a net cash position in the next 12 months, significantly de-risking the balance sheet and providing optionality for M&A or capital returns.

Fears of a contract non-renewal or change of administration are overstated. The company’s successful track record of execution suggests that the new contract extension will continue to be renewed annually; a change to a Republican administration and stricter immigration policies might actually create more migratory flows, a benefit to TH.

Company Background

Target Hospitality (TH) is a specialty rental provider of modular housing and services (i.e. man-camps) operating in the government and oil & gas sectors with ~16,000 beds across 27 communities. The company provides lodging as well as turn-key ancillary services including catering, recreational activities, health care, and others.

Over the past 3 years, the company has increasingly focused on securing government contracts, seeing a need for the temporary housing of migrant children and families. TH generated $291m in revenue in 2021 and $119m in EBITDA.

Target Hospitality was formed in 2019 from the combination of Target Lodging (spun out from Modulaire Group) and Signor Holdings and brought to market through a SPAC. The prior majority owner, TDR Capital, still controls approximately 67% of the common. TDR Capital has a solid track record of value creation, having also brought Willscott Mobile Mini (WSC), a specialty rental company, to market via SPAC in 2015.

Investment Thesis:

I recommend an investment in the equity of Target Hospitality at $11.73 per share for the following reasons:

1. The market has not appreciated the transformative nature of TH’s recent government contract win.

On July 6, 2022, Target Hospitality announced a major expansion to an existing contract with the US government in which TH provides housing and services for a population of unaccompanied minors awaiting migration proceedings in the US. The contract extension calls for an increase in the number of beds in West Texas to 6,400 from 4,000 and major infrastructure upgrades to support the increase in population. The new contract has three components. First, TH will be paid $196m in annual payments for the leasing of the facilities. Second, TH will receive up to $185m for the ancillary services provided (payouts will depend on the utilization levels of the facility). And third, TH will receive a FULL reimbursement of the CAPEX that will go into upgrading the facilities (this will be a one-time payment of $194m). The contract is incredibly lucrative for TH. I estimate that the cash gross margin of this contract will come at ~70% (assuming leasing margin at 80% and services at 55%). With little incremental OPEX required at the corporate level, this new contract is to add $200m in incremental annual EBITDA. Given the company’s minimal CAPEX needs (maintenance CAPEX is 1-2% of revenues or about $12m/year total), this should convert meaningfully into free cash flow. Prior to this, the company had originally guided 2022 EBITDA to $130m. With no additional improvement to the underlying oil & gas business, this new contract puts Target Hospitality at a run-rate EBITDA of over $330m vs. a current enterprise value of $1.5B (excluding the one-time benefit of the CAPEX reimbursement). Despite the stock re-rating from under $5 to approximately $12 today, the market has clearly not priced in the new contract.

2. By pivoting away from oil & gas, TH has become a much higher quality business than the market gives it credit for.

The new contract will take government revenue to over ~70% of the total. This means that the market should start to see Target Hospitality as a much higher quality business given: 1) significantly decreased volatility in both revenues and cash flows (as they will no longer be so exposed to the highly cyclical oil & gas industry), 2) greater visibility of revenue and earnings from having long-term contracts and minimum revenue commitments (most revenue will be at contracted prices rather than at spot rates), 3) improving unit economics and a higher return on invested capital as government contracts carry higher margins and reimburse the company for growth CAPEX. Given these changes, I expect that the market should reward TH with a higher multiple over time.

3. The risk of a contract non-renewal is overstated.

One of the reasons the stock price might not fully reflect the magnitude of the new contract is that it sees it as non-recurring. The terms of the new contract call for one year with an additional 6-month extension. While there might not be immediate visibility beyond that timeframe, there are a few reasons why I believe this contract will be recurring in nature.

First, the government is spending close to $200m in CAPEX on a facility that is highly customized for children’s needs. The amount of money being spent indicates that the government views the West Texas facility as a long-term project. Secondly, the company has a history of successfully working with the government and extending contracts past their initial terms. The Dilley facility in Texas, which serves a population of women with children, has been operating for over 8 years, although this originally started as a one-year project. Noteworthy, this contract operated across the Obama, Trump, and Biden administrations with no interruption, and the contract now operates under 5-year extensions. Third, the contract expansion awarded to TH was a sole-source contract (i.e. not open to other bidders), which means that the government saw no other company capable of offering the level of quality, service, and price that Target Hospitality (and Family Endeavors, its non-profit partner) could provide. Last, the West Texas facility was selected by the government as one of only two facilities to shift the designation from an Emergency Influx Site (EIS) to a permanent site. While EIS locations are used to temporarily accommodate surges of unaccompanied minors, permanent sites are intended to house the migrant children on a full-time basis. It also means that permanent sites will be prioritized over EIS locations, raising the level of utilization for those facilities.

Importantly, federal funding for both FY 2022 and 2023 also looks to be secure. For FY22, the UC (Unaccompanied Children) Program appropriated $8.8B to fund the potential need for up to 19,000 beds. For FY23, there is a request in the budget for a contingency fund that automatically disburses funds to activate and acquire additional bed capacity if needed. At the current expected level of referrals (150,000), the contingency fund would pay out an additional $4B to the UC program.

4. A change to a Republican administration could increase the need for the housing of unaccompanied minors and families, a net positive for Target Hospitality.

A tougher stance on immigration is likely to create more migration of unaccompanied minors. Unaccompanied minors are a protected class under federal law (Title 8), which explicitly disallows policies that turn away children that arrive at the border unaccompanied by a parent or legal guardian. Despite any changes to general immigration laws, migrant children seeking asylum status will continue to be exempted from these more restrictive laws because of Title 8 protection. We can therefore expect that unaccompanied children will continue to arrive in the US and that there will be a consequent need to provide them with housing and assistance. In case of stricter policies, where adult asylum seekers are prohibited from coming into the US to request asylum, more migrant families will likely make the tough choice of self-separating at the border (i.e. sending children unaccompanied to make the crossing); for this reason, restrictive policies are more likely to increase rather than decrease the number of unaccompanied children coming to the US.

For context, in 2020 the Trump administration stopped immigration to the US using Title 42, which permitted border officials to send migrants back in the interest of protecting public health (due to COVID). Unaccompanied minors, however, were exempted from this policy starting in November 2020. Record arrivals of unaccompanied children soon followed (as seen in the graph below). I expect that a change to a Republic administration could lead to another such scenario.

5. Risk reward is very attractive with an expected 3x win/loss skew. My bear case suggests minimal downside at a PT of $8/share relative to my base case PT of $22/share.

Target Hospitality is very cheap on both an absolute and relative basis. On an absolute basis, TH is trading at a FCF yield (FCF/EV) of 18% on my 2024 FCF estimate ($265m) and at 4.4x 2024 EBITDA on my numbers ($340m). [Note: 2023 numbers will be artificially high as the CAPEX reimbursement will flow through the P&L as revenue.] TH has historically traded at a range between 5.0x to 8.0x EBITDA. TH is also trading at a wide discount to peers. Although TH is a higher quality company than pureplay government service providers such as GEO and oil & gas specialty rental companies like CVEO, it is trading at a discount to both; these companies currently trade at 6.8x FY2 EBITDA and 6.0x FY2 EBITDA, respectively.

For my bear case (PT of $8), I assume that the government extension contract is not renewed past its initial 18-month period and that EBITDA consequently declines to a run rate of $130m for CY24. I do assume, however, that the cash generated from the contract, combined with the government’s CAPEX reimbursement, allows the company to pay down the $340m in senior secured notes and the remainder of the ABL facility; TH ends FY23 in a slight net cash position. I then value the company a 6.0x EBITDA multiple, which is right in line with its historical average and compares to its lower quality peers, despite being a better business with a clean balance sheet (and $40m in interest expense savings that accrue directly to the equity).

For my base case (PT of $22), I assume that the government extension contract is renewed indefinitely and that the oil & gas operations continue to improve slightly, with slight increases to ADR (trending up to $82/night, and still below 2019’s $84/night) and a flat level of utilization at 75% (relative to pre-COVID). Like in the bear case, the company pays down its debt and ends FY23 in a slight net cash position. I expect the company to generate approximately $340m in EBITDA (or ~$265m in free cash flow), to which I apply a 7.0x EBITDA multiple. My valuation imputes a free cash flow yield of ~10.5% and a P/E multiple of ~12x, valuations which do not give much credit for potential growth opportunities.

6. There can be additional upside from either: acquisitions, a capital return program, continued recovery in O&G, and/or further government contract wins.

What makes the risk/reward so attractive is that TH will be able to, with near 100% certainty, de-lever its balance sheet and go into a net cash position within the span of ~12 months thanks to this new contract extension. Coming out of this, the company will be in a much stronger position to pursue value accretive opportunities, such as larger scale M&A or a potential return of capital program for investors (the company has done little in the way of repurchases or dividends since it came public.) Management has expressed interest in making acquisitions to diversify their end-industry and contract exposure, but they remain open-minded to repurchases if they see a good opportunity to return cash.

Moreover, the remaining 30% of revenue that continues to have exposure to oil & gas could also prove attractive if we see a structural improvement in the US oil industry to pre-covid levels. Rig counts in the Permian Basin (a good proxy for utilization of TH’s beds) remain notably lower than in 2019 despite much higher crude prices. However, if energy prices are expected to remain elevated, energy companies are more likely to make investments to increase drilling capacity, which would increase demand for TH’s services. Returning to 2019 average utilization (~6,700 beds) in the Permian Basin, for instance, could add an incremental $30m in EBITDA per year for TH.

Lastly, the company outlined its intention during the latest earnings call to double its revenue to $1B through additional contracts in either government services or in oil & gas. However, given the continued need for humanitarian services and a consistent track record of execution, I believe management will be able to keep landing new contracts that can leverage its expertise in facilities construction, management, and value-added services.

Summary Model

Investment Risks / Where I could be wrong:

The new contract extension significantly increases customer concentration (the government will represent +70% of revenue). There is a risk that the government could choose to not renew the expanded humanitarian contract (the West Dilley contract is covered under five-year extensions).

Humanitarian contracts require annual budget appropriations. In a change of administration, there is the risk that the new administration might simply cut off funding for these programs. However, you must consider the optics of such a move (no political party wants a front-page cover story about minors being held in less-than-ideal facilities).

My 2023/2024 base case estimates assume that the new 6,400 bed extension will ramp up to 100% utilization. While I believe this to be a reasonable assumption (all other projects have operated at 100% utilization rates non-stop), it’s no guarantee.

Rig counts in the Permian basin do not recover and/or decrease. Capital spending remains low due to investor pressure for capital return rather than capacity expansion, resulting in little need for more man-camp space.

Any comments/feedback, please write to me on Twitter @clarksquarecap. Thanks!

Edit (10/24/2022): Attaching my model in case it’s helpful.