Three-minute pitch #12

Another cheap remainco opportunity

EDIT: Closed this out in November 2024 at CAD 0.36 for a slight loss of ~6%.

Welcome back, Ultimate Value readers!

Today, I have an interesting Canadian microcap.

I know, I know. Canada? It trades on the Venture exchange? Might as well be investing in frontier markets.

But this opportunity looks enticing because this company sold off two divisions, and the remainco is a much better business.

Best of all, the stock now trades at a significant discount to public peers.

Let’s take a look.

Company: Quisitive

Ticker: QUIS.V (Canadian Venture Exchange)

Price: CAD $0.385 / USD: $0.28

Shs O/S: 273m

Mcap: USD 76m

ADTV: USD 75k

USD/CAD: 1.38Sometimes, the market is slow to recognize a situation where a business has completely transformed itself overnight.

Quisitive (QUIS.V) is such an opportunity [disclosure: I own shares].

Quisitive is a Canada-headquartered roll-up of IT consulting firms. Over the last few years, the company has attempted, without much success, to enter the competitive payment space. Last October, investors revolted and tried to replace three members of the Board. This was unsuccessful, although the company compromised by adding two new members, Nick Lim (FAX Capital, previously BAM) and Darcy Morris (Ewing Morris & Co. Investment Partners).

Following this addition, Quisitive announced a strategic review and, consequently, the sale of its two payment-focused businesses.

On November 28, 2023, Qusitive announced the sale of PayIQ. Terms included QUIS rolling its equity stake into preferred shares worth $27m (puttable in 3 years) and earn-outs worth a maximum of $18m.

On March 27, 2024, Quisitive announced the sale of BankCard for a cash payment of $40m, the return (and cancellation) of 133m shares in QUIS, and a release from an existing $10m earnout.

Following the divestment of these two businesses, we are left with a:

Market cap of $76m USD (273m shares outstanding x $0.28 USD/share)

Cash of $5m and debt of $34m

An investment of $27m in PayIQ preferred equity and up to $18m in earnouts.

This means that pro forma for the PayIQ stake, the stock is trading at an enterprise value of $78m, with management guiding to $16.5m (at the mid-point) of EBITDA in 2024, or roughly 4.7x EBITDA without giving any credit to potential earnouts. Assuming $10m in earnouts, the multiple could fall as low as 4.0x EBITDA.

So what does Quisitive do?

Quisitive is (now) a pure-play Microsoft-focused IT consulting and managed services provider. The company specializes in helping mid-market companies adopt cloud services such as Azure/Microsoft 365/Dynamics 365 and provides ongoing support. Approximately 40% of revenue now comes from recurring revenue, with QUIS also offering a few custom SaaS applications.

My thesis is as follows:

This is a much better business, and the market hasn’t given it any credit yet.

Business simplification: Analysts can now more easily compare QUIS to other consulting businesses and apply a commensurate multiple

Reduced CAPEX: before the sale, the PayIQ business required about $5-6m in annual CAPEX, which is no longer needed. The consulting business (remainco) requires little CAPEX and should readily convert EBITDA into free cash flow.

The company’s balance sheet is in much better shape: the $40m cash payment for BankCard brought down net debt to ~$30m, or ~1.7x leverage vs. 2.6x prior.

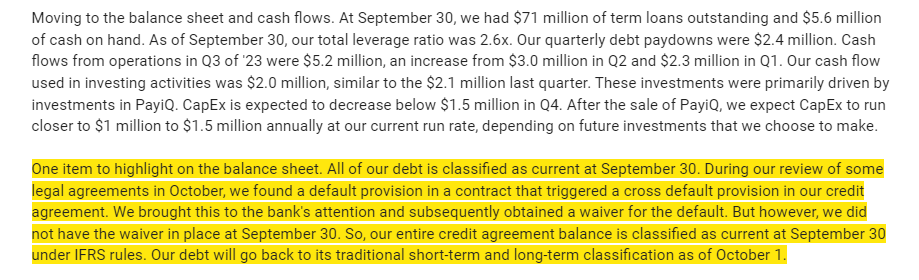

Importantly, QUIS solved an issue where the entire debt was considered current under IFRS accounting due to a technical issue that has since been remedied.

The business has transformed itself quickly, but it doesn’t yet show up in the numbers.

There are a few meaningful items that will take a few quarters to be reflected in data services, such as 1) the correct share count (133m shares are to be canceled, so the current market cap shown by most providers is wrong), 2) the debt paydown, 3) the preferred stake in PayIQ will also not likely be reflected in EV calculations unless you are looking at this directly.

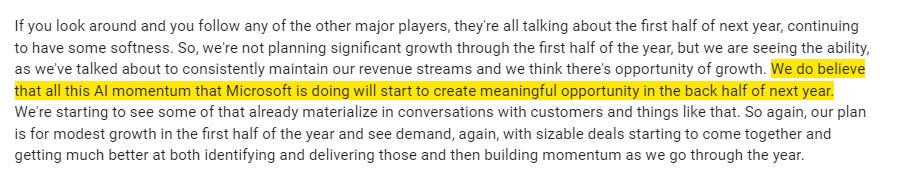

Revenue could re-accelerate, given the increasing interest in AI applications. QUIS is well positioned with its Microsoft partnership/offerings.

Consulting revenue slowed down meaningfully in 2023 as cloud providers faced a more challenging economic environment this past year. However, QUIS noted on the Q3 call that they have seen revenue stabilize (a +1% QoQ increase).

In the next few quarters, QUIS could see a re-acceleration in top-line as customers leverage QUIS’ offerings to add AI capabilities to their tech stacks.

QUIS has mentioned that, based on conversations with their customers, they see “AI momentum” creating meaningful opportunities in the back half of ‘24.

Management’s guidance for 2024 looks beatable.

Management laid out a pro forma guide for $16.5m in EBITDA for FY24.

However, the guide looks sandbagged, given significant cost cuts starting in Q1/Q2 of this year. LTM EBITDA is at $15.9m, but on the Q2 call, management stated that if they had implemented these cost cuts at the beginning of the year, 1H23 EBITDA would have been $3.5m higher. So, on very rough numbers, the consulting business should be generating ~$20m on a run-rate basis.

For FY24, I assume that QUIS returns to growth in the back half of the year (+4% YoY) and reinvests some of the margin (GMs from 43% to ~40%) to grow their AI offerings, which gets me to about ~$20m in EBITDA. This is ~20% higher vs. the company’s guidance. At $20m in EBITDA, the stock would be at ~4.0x EBITDA.

Putting it all together, you have a nice little consulting business at ~4.0x EBITDA. I am no expert in IT consulting, but this does not feel like the right multiple to me.

At the very least, this should be worth a “no growth” multiple. At 7.0x EBITDA (which imputes a ~12x P/E multiple), the stock would be worth CAD $0.70, or about 80% above the current market price.

Consulting peers tend to trade at ~11x EBITDA, with a wide distribution depending on size and quality; however, the low end seems to be around 6-7x EBITDA. So, 7x seems right to me.

If QUIS can reaccelerate, I think the company could be worth another 1-2x additional turns. At 8.5x, the stock could be worth about $0.84 CAD (about 120% upside).

For all the above reasons, I am LONG QUIS.V.

Thanks so much for reading! Let me know if you have any thoughts, questions, or pushback in the comments below.

Anything on the management's incentives and skin in the game?

Thanks for the idea. And I appreciate that as a Quick Pitch you aren’t claiming to have done all the work!

1. The $27m pref: is the entity to which Quisitive can Put good for the money? If not, this investment could still be a zero. It can’t be deducted from EV without a mighty discount without understanding that. What are the other terms of the pref please, eg does it pay cash interest? There is reference in a slide footnote to the $27m being adjustable.

2. How can we roughly get remainco “ebitda” into something real. Little capex one hopes, but maybe they are capitalising some development; how much of the SBC is real and ought to be deducted; there’s nearly $2m depreciation but that includes the payments businesses, etc.