Three-minute pitch #14

+50% grower at an extremely low valuation.

Hello, Ultimate Value readers!

I am back with a new idea today. Here are some of the takeaways:

Extremely under-the-radar, with no public write-ups.

US-listed, with a market cap of ~$90m USD.

ADTV over the past 3 months has been $2.7m (although most volume shows up during earnings).

Revenue growth has accelerated and exited Q4 at a +50% YoY growth rate.

It’s very asymmetric. Over 80% of the market cap is in net cash, and the business is valued at 0.2 EV/sales.

At a 1x EV/sales multiple, this could have a +100% upside over the next 12 months.

Let’s take a look.

Company: MoneyHero

Ticker: MNY

Stock price: USD $2.01

FD Shares O/S: 44.9m (excluding OTM warrants)

Market cap: $90m

Net cash: $69m

EV: $22mMoneyHero (US: MNY) [disclosure: I own shares] is an online lead generation and marketing services firm for financial products in Southeast Asia. The company is dually headquartered in Hong Kong and Singapore. In late 2023, MNY came to the US market via SPAC with support from reputable firms, including Thiel Capital and Richard Li’s Pacific Century Group (PCG), raising $100m in gross proceeds.

Most of MoneyHero’s revenue comes from its comparison offering. MNY operates websites that educate consumers on relevant financial products such as credit cards, insurance, and wealth management (like NerdWallet/Credit Karma or a Moneysupermarket if you are in the UK). Customers who sign up for financial products via MoneyHero earn rewards—for example, a Dyson Vacuum for successfully applying for a credit card.

Credit cards make up ~70% of the company’s revenue, but the company has been moving into high-margin products such as insurance. MoneyHero is partnered with 280 financial institutions (Citi, etc.), where it acts as an effective customer acquisition funnel. Importantly, MNY is well-aligned to deliver positive outcomes, as 90% of revenue is tied to approved financial applications.

While online lead generation can be a competitive business, a few things should make MoneyHero a more durable business than meets the eye. First, MNY is the largest online lead-generator in Asia, with a presence in multiple countries. Second, MNY has a leading market share in 4 out of 5 markets in which it operates: Singapore, Hong Kong, Taiwan, and the Philippines. Lastly, approximately 75% of the company's customers come via organic channels — i.e., unpaid traffic — as it has developed well-known brands in each region.

Why is this opportunity available?

Non-fundamental selling: One investor in the SPAC was guaranteed a return (5%) by the sponsor, which had to be satisfied by the sponsor selling shares in the open market.

Ex-SPAC: Most investors are unwilling to look at these opportunities.

Messy financials: 2023 reported numbers are quite messy, so you have to look at pro-forma numbers.

Microcap: a market cap under $100m makes this better for small funds, etc.

I think MoneyHero is a compelling investment for the following reasons:

Revenue growth inflected in Q4, with +53% YoY growth following a period of LDD growth as the company prioritized getting to profitability.

MoneyHero began making strategic investments in Q3 with higher payouts to consumers to take share from competitors. This resulted in an acceleration in revenue in Q3 and even faster growth in Q4.

I expect fast growth to continue as the “comparison” business benefits from further growth in insurance products, which is growing triple digits. Moreover, the company’s B2B business (Creatory — a platform that connects influencers with financial partners) is growing at a triple-digit rate and is already >20% of revenue.

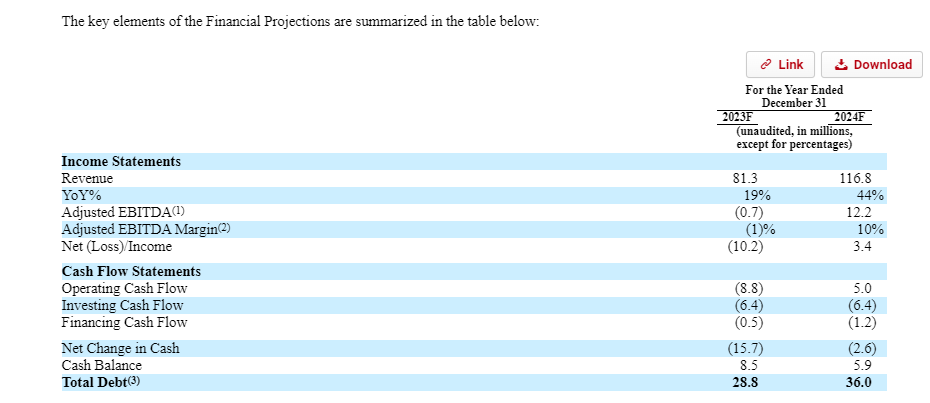

MoneyHero is guiding revenue to “above $100m” for 2024, implying +24% growth. MNY will likely beat this conservative (i.e., sandbagged) target.

In the Estimates shared in the original prospectus—filed in September 2023—management projected 2024 revenue at ~$117m.

In the Q3 earnings call, management noted that October and November, which are not seasonal months, averaged $9m in revenue. This would imply a run-rate revenue of ~$110m.

MNY’s Q4 revenue was at +50% growth. Getting to a ~20% growth would imply a steep deceleration for the rest of the year.

A new CEO joined in February, so there is an incentive to set a low guide to beat it throughout the year.

MoneyHero will become adjusted EBITDA breakeven this year. As the company hits breakeven, I expect the shares to re-rate.

Management is guiding to adjusted EBITDA breakeven by the back half of 2024.

Some markets are already profitable, including Hong Kong and the Phillippines.

As market participants observe that MNY can be profitable, I expect they will bid the stock to a “real” multiple.

From the Q4 earnings call

Valuation is very compelling. The big cash pile protects the downside, making this a good asymmetric bet.

MNY has no debt, just a net cash balance of $69m relative to a market cap of $90m. Cash covers almost 80% of the market cap.

Assuming $110m in 2024 sales, I see MNY trading at 0.2x EV/Sales.

Peers trade at much higher multiples:

Nerd Wallet (US: NRDS) trades at 1.5x NTM sales

Moneysupermarket (UK: MONY) trades at 3.0x NTM sales

At a discount to peers, a 1x sales multiple, I see shares at $4.00 a share, or a double from the current price.

Management believes in the “mid-term,” they will see adjusted EBITDA margins in the 5-10% range. At 1x sales, it would imply a ~13x normalized EBITDA multiple.

Model:

Catalysts:

MoneyHero reaching breakeven margins this year.

Risks:

MNY is spending aggressively to take share from competitors. There is no guarantee that this will yield a good return on the money spent.

MoneyHero relies on search engine traffic and SEO/SEM, which is a risk.

FX risk. MNY reports in US dollars but is exposed to multiple currencies.

MNY is a controlled company through a dual share class structure (owned by Richard Li) - 30.6% equity interest and 78% voting power.

Thanks so much for reading! Let me know if you have any thoughts, questions, or pushback in the comments below.

Great cash pile. But they're burning through that cash like crazy. I don't think it offers much downside on a forward-looking basis

This sounds great and as you say, the cash protects the downside. But is the target price realistic? 13x EBITDA is a) well above MONY 9.4x fwd / NRDS 7.5x fwd which could need justification b) at such narrow EBITDA margins, would there even be real profits/cash flows (there's probably SBC, some capex even if they expense software, office leases not in EBITDA, etc.). Maybe there's something about their markets which prevents a properly-profitable lead-gen website working?