Three-minute pitch #2

Asset sales leave behind the company's crown jewel (at a big discount!)

Yesterday, a company in the UK announced that they are selling their main business and retaining their crown jewel software business. This allows investors to buy into a high-quality business at a steep discount to peers.

There is potential for the stock to run once the details of the transaction are fully digested. But, I think there’s enough here for this to be a compelling long-term story. Here’s a quick pitch in the interest of timeliness.

The opportunity we are looking at today is Pendragon (LSE: PDG). The stock is trading at 23.7 pence per share (disclosure: bought some shares today.)

Pendragon is a GBP 330m small-cap in the UK with three businesses: 1) an automotive dealership group with 140 dealership sites, 2) a vehicle leasing business, and 3) a SaaS business, Pinewood, that provides dealer management system (DMS) software.

Now, what’s interesting is that yesterday, the company announced that Lithia Motors will be acquiring the dealership and leasing businesses.

This will leave behind the better SaaS business as part of the publicly listed entity. Moreover, Lithia Motors and Pinewood will team up to create a JV in the United States in which Pinewood can target Lithia’s existing dealership network (~300 dealerships) as well as incremental opportunities within the country.

The terms of the transaction were as follows (note, the per-share valuations were determined by PDG/Lithia)

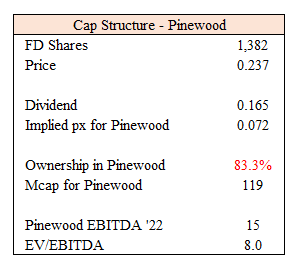

From the proceeds, PDG holders will receive a 16.5 pence/share dividend.

PDG holders will retain 83.3% of the continuing business, which includes Pinewood (valued at 10.3 pence/share)

Ownership in the Joint Venture (valued at 0.6 pence/share).

The implied value of the pieces totals 27.4 pence/share (recall that the shares are at 23.7 pence/share).

Netting out the dividend, the implied price for the remainco (aka Pinewood) is 7.2 pence/share (which will own 83.3% of Pinewood). Therefore, the implied market cap/EV for Pinewood is 120m GBP. Importantly, Pinewood will have no debt or pension liabilities - those will be assumed by Lithia in the transaction.

Pinewood looks to be a good asset. Here are some highlights:

Very high margins: +90% gross margin, 60-70% EBITDA margins.

Sticky, recurring revenue (90% is recurring) with low customer churn (2% average customer churn per year)

Approximately has ~20% of the UK market. In total, there are 30,000+ users.

Now, at a market cap/EV of GBP 120m, this transaction essentially lets you buy a high-quality SaaS business at ~8.0x 2022 EBITDA (~15m in 2022 EBITDA). This is cheap on a headline basis. Pinewood has laid out a target to reach GBP 27m in EBITDA by 2027. This would imply a valuation of 4.4x EBITDA on ‘27 numbers.

However, this still does not give any credit to the incremental opportunity that is created by the new partnership (see slide below). In the JV, Lithia + Pinewood will have access to another 17,500 of Lithia’s customers. At the current ARPU of ~800 GBP and at an incremental margin of ~70%, this means another possible GBP 10m in EBITDA (of which Pinewood would get half, or 5m GBP). This does not factor in other US customers that might be signed up. Over time, I expect that the US could become a big earnings driver if the company is successful.

So what should this be worth?

Here’s a very rough back-of-the-envelope analysis. I lay out the three ranges of EBITDA: 15m / 27m / 32m GBP. Comps typically trade at 15-25x EBITDA. I use 15x for conservatism. We don’t need to be overly precise to see that there is a mispricing. If we assume the company can come closer to 20m in 2024, then the Pinewood stub should be worth roughly 18 pence/share, or an incremental 11 pence to the share price today. The downside is well protected in the interim given the upcoming dividend/cash payment.

Putting it all together, you have a good, very profitable SaaS business trading at <8x EBITDA. I like the risk/reward from here but keep in mind that there are risks. Timing-wise, the transaction is to be completed in Q4 2023 and is subject to shareholder and regulatory approval.

That is the 3-minute pitch! I put this together very quickly so please excuse any grammar issues/typos.

Here are some good resources to get you up to speed.

Good VIC write-up from May 2022 highlighting the SOTP value

Pendragon 2022 Annual Report

Thanks so much for reading! Let me know if you have any thoughts, questions, or pushback in the comments below.