Updates: January 17, 2024

Updates on: TRST.LN and WCG.AX / 5GN.AX

Hello, Ultimate Value readers!

I hope everyone is having a nice week.

I have updates on Trustpilot (TRST.LN) and on Webcentral (WCG.AX / 5GN.AX).

Let’s take a look.

Trustpilot - Risk/reward more balanced

I first wrote up Trustpilot (UK: TRST) back in August at a price of 91p. The stock has done well and is now trading at 163p (+79%).

Check out the original write-up and the most recent update below:

Last week, Trustpilot released a trading update for the year ending December 31, 2023, which exceeded expectations on both top and bottom lines. With shares trading at 163p, TRST now has a market cap of $844m USD and an EV of $753m (~$90m of net cash).

The company experienced strong continued operating momentum. Key highlights for FY23 included:

Revenue +17% cc YoY

ARR + 18% cc YoY

Total bookings +16% cc YoY

Net dollar retention rate YoY at 99% (FY22: 100%)

Most importantly, TRST continues to deliver operating leverage. Adjusted EBITDA for FY23 is to come in at the top end of the range of expectations, which implies USD ~13-14m (7% EBITDA margin).

From here, I expect Trustpilot’s strong operating momentum to continue. While the shares have started to appreciate meaningfully, I think there should still be enough upside to make holding the shares worthwhile. I estimate that Trustpilot could generate $255m in revenue and $45m in EBITDA in 2025, which would put shares at <3x EV/sales and a ~17x adjusted EBITDA multiple (at 30% steady-state margins, this would be ~10x EBITDA).

Given the company’s strong competitive position in markets like the UK, as well as the company’s attractive unit economics, I believe that these multiples are still reasonable, if not cheap. If you don’t factor in any additional multiple expansion, you would still be able to earn an IRR in line with earnings growth, which is to be significant given top-line growth (mid-teens plus) and continued margin expansion (steady-state margins likely in the ~30% range).

Lastly, sell-side estimates still look very beatable over the next 12-24 months. The sell-side is modeling ~15% incremental EBITDA margins for FY24/FY25, while I think this should be at least in the 30-40% range. I think EBITDA will come in much higher than consensus.

Given strong operating momentum and a reasonable valuation, I remain LONG.

Webcentral - Risk/reward more favorable

I originally wrote up Webcentral (previously WCG.AX, now 5GN.AX) back in late October when the stock was trading at ~0.245 AUD per share. The stock is now trading at ~0.20 AUD per share, down ~18% since entry.

Please refer to the original write-up here:

There have been several developments since then, and I thought revisiting the idea with a few more thoughts would be timely.

Overall, I find the idea is still compelling, and I have added to my position at a price of ~0.20 AUD/share.

Since I first shared the idea, the most important developments have been:

The sale of the Webcentral assets has been completed. Due to greater transaction expenses, proceeds were a few million less than I expected. I estimate a pro-forma cash balance of ~$81m AUD (vs. $84m expected).

Webcentral changed its name to 5G Networks and its ticker to 5GN.

5GN announced a share repurchase of up to 33m shares (about 10% of shares outstanding, excluding options).

5GN announced a dividend of $0.02 AUD (~10% yield vs the current price).

5GN announced the acquisition of a small cyber security company for $4.5m AUD (roughly $3m in cash and $1.5m in stock). 5GN is paying 3x EBITDA.

So, where does that leave us today?

5GN has three components of value:

The net cash pile: roughly ~$79m AUD after cash payment for the acquisition.

The 1/3 stake in Webcentral which was marked at ~$20m AUD.

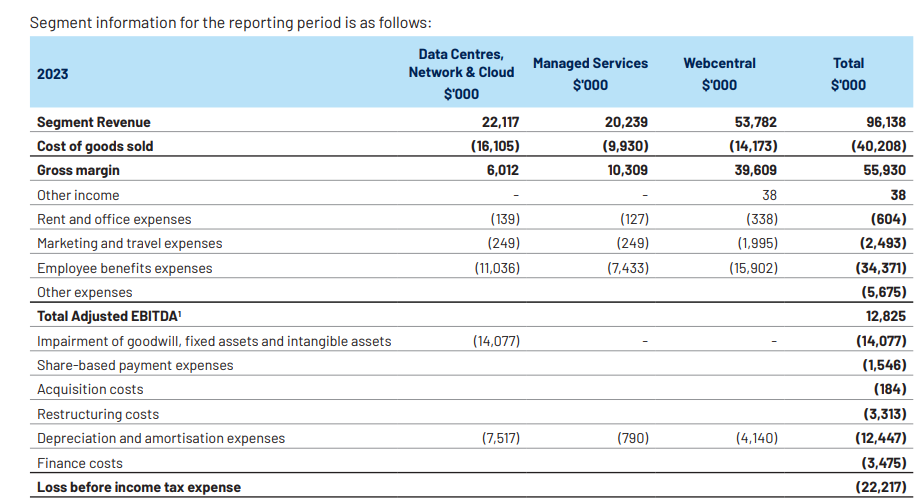

The 5GN business remainco (data centers + managed services), which should generate ~$45m in revenue in FY24 + a recently acquired cyber security firm that will add ~$4m in revenue and ~$1m in EBITDA.

In my initial assessment, one thing I missed was that the $5m net profit figure includes interest income (from the ~$80m in cash) as well as minority interest from the remaining 1/3 stake in Webcentral.

This would imply that 5GN (the remainco) has break-even operating earnings at best. More likely, the remainco is slightly loss-making. If we allocate corporate overhead (other expenses) on a proportional basis, the remainco would have lost c. $5m in EBITDA in FY23.

I would expect 2024 to be better for the 5GN business for a couple of reasons. First, they signed a $12m cloud service agreement with Webcentral, which has a minimum spend of $4m for the first year. Given spare capacity, the incremental margins on this agreement should be very high, perhaps as high as 70-80%. Second, the company recently announced its intention to purchase a cyber security business at 3x EBITDA, which will add another $4m AUD in revenue and roughly $1m in EBITDA. In addition to some organic growth and expense rationalization post-divestment, I think 5GN should roughly break even on an adjusted EBITDA basis.

I estimate that there should be another $4-5m between maintenance capex and lease costs (in cash), which means the company will be slightly FCF negative in the interim, although it will have cash coming in from the large cash balance that will offset this. However, I think the company might be able to find more tuck-in acquisitions at low multiples and leverage its existing infrastructure to get to positive EBITDA and FCF over time. A larger deal might get it to a good level of profitability, but that obviously comes with risks.

Putting it all together, I believe the stock should be worth at least 35c (vs. 20c currently) per share, with the value coming from:

Net cash of $79m AUD ($0.215 AUD/share)

The 1/3 equity stake in Webcentral, worth $20m AUD ($0.06 AUD/share)

$50m AUD of revenue at 0.5 EV/sales ($0.07 AUD/share)

My price target is lower than previously, primarily due to 1) using a low(er) revenue multiple on the remainco instead of a “multiple” on net profit, 2) adjusting the cash balance, and 3) factoring in dilution from stock options.

The value of the first two components should be straightforward. I am not certain that the market will give #3 much value in the near term, but I do think you should be well protected given the significant asset values of #1 & #2.

In the meantime, I think there are catalysts that could drive the stock, including:

A publication of half-year financials (with a run-rate revenue/earnings for 5GN and a net cash balance)

Full-year guidance for FY24

The start of the company’s buy-back program (~10% of shares max)

The upcoming dividend payment (~10% yield)

Announcement of prudent M&A deals

Given the significant margin of safety, incoming cash returns (dividend + repurchases), and a chance for upside if the company is able to execute on attractive M&A deals, I am LONG.

Note: I assume a total share count of 365m shares. 342m outstanding shares + 7m shares issued for the acquisition + 15m of net dilution from stock options (treasury method; 60m options, strike AUD 0.26, exercised at AUD 0.35).

Thanks so much for reading! Let me know if you have any thoughts, questions, or pushback in the comments below.